The plastic waste problem

Large amounts of plastics are still being produced each year - 359 million tonnes in 2019.1 In addition, the development and introduction of new plastic materials and formats across the globe is happening far faster than the development and rollout of corresponding after-use systems and infrastructure.2 The objects that we separate and put in recycling bins are often not recycled. This is a waste in two senses of the word: both as harm to the environment and as a loss of value when we discard a material that could otherwise have been re-used, either through re-use of the product itself or as input material for new products after recycling.

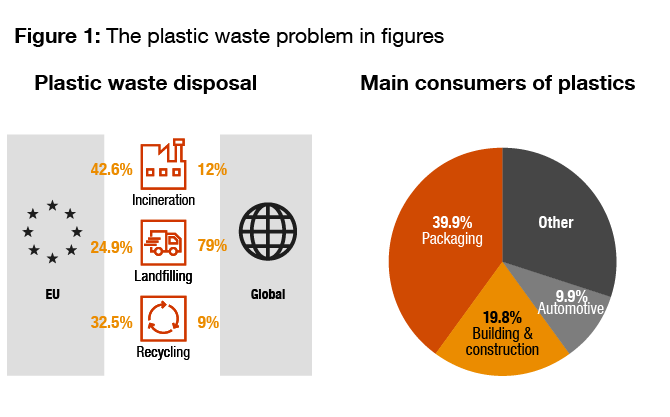

In Europe just above 30% of the 29.1 million tonnes of plastic waste generated every year is collected for recycling.3 Instead 43% of plastic waste in Europe is incinerated, and one quarter is still being landfilled.4 A substantial proportion of plastics ends up in the sea, and in a business-as-usual scenario, there would be more mass of plastic than of fish by 2025.5 The carbon footprint from plastics would be 15% of the global annual carbon budget in 2050 (up from 1% in 2016).

Even if current recycling rates continue to grow linearly, 56% of the estimated plastic waste will still not be recycled in 2050.6 In terms of cumulative amounts, if we also assume that plastics production and waste generation follow their historical trends, then 65% of plastics ever produced will not be recycled by 2050.7

1PlasticsEurope (2019), Plastics - The Facts 2019.

2The World Economic Forum (2016), The New Plastics Economy Rethinking the future of plastics.

3European Commission (2018), A European Strategy for Plastics in a Circular Economy.

4PlasticsEurope (2019), Plastics - The Facts 2019.

5PwC (2019), The Road to Circularity.

6Geyer et al. (2017), Production, use and fate of all plastics ever made.

7Ibid

Failures of the plastics market

From an economic perspective, if left alone, the market will not solve the problem of plastic waste. The true costs of conventional plastics to society - through climate change and environmental degradation - are not reflected in its current price. As the price of oil - the feedstock for plastics - has hit record lows since the Covid-19 induced global recession, this problem has become even more acute.

Under today’s market conditions, it is difficult for plastics manufacturers to capture the price premium that end consumers would be willing to pay for sustainable plastics, and pass that margin up the value chain. As a result, negative externalities, coordination problems and high transaction costs all persist on the plastics market. Policy interventions will be needed to solve them.

The scheme below sets out some of the market failures and the interventions that can solve them.

Examples of problems on the plastics market

- Recycling of conventional plastics

- Low demand for recycled plastics

- Bioplastics is not a silver bullet

Recycling of conventional plastics

Recycling is one approach to solve the plastic waste problem, but has thus far been supply-side driven and focuses mainly on collection and recycling rates.8 The EU has a strategy to improve collection and aims to recycle half of its plastics by 2030.9 Yet, this approach alone does not seem to be working: increased collection rates have not translated into more recycled content in products.

8EU Waste Framework Directive (2008), Directive 2008/98/EC.

9European Commission (2018), A European strategy for plastics in a circular economy.

Low demand for recycled plastics

There are technical difficulties related to recycling and recycled plastics. Plastics is not one homogeneous material. There are thousands of different plastic materials, each with different properties that make it suitable for different uses, but which also makes it harder to recycle or re-use. As a consequence, the quantities of plastics being recycled remain small, and recycled plastics are often of a lower quality than the virgin plastic equivalent, i.e. it is being downcycled. Those same concerns also mean that recycled plastics cannot compete on the global market: industrial buyers require large amounts and high quality standards. All in all, it is cheaper and more efficient to make plastics from virgin feedstock. As a result, today only 6% of the total plastics demand globally is for recycled plastics.10

10European Parliament (2018), Plastic waste and recycling in the EU: facts and figures.

Bioplastics is not a silver bullet

Bioplastics are plastics that are bio-based, i.e. either fully or partly made from natural resources, such as sugar, starch, biomass, and/or they are biodegradable.11 However, not all bioplastics are recyclable12 and the degree to which bioplastics plastics can be composted depends on environmental conditions, such as temperature, humidity, pH value or oxygen contents, but also on structure and composition of the specific bio-plastic material. The European Commission has actively supported the development of bioplastics13 and the Green Deal contains initiatives to develop a regulatory framework for biodegradable and bio-based plastics as a first step to overcome these problems.14

11European Bioplastics (2016), Fact Sheet.

12Soroudi and Jakubowicz (2013), Recycling of bioplastics, their blends and biocomposites: A review.

13European Commission (2017), Bioplastics: Sustainable materials for building a strong and circular European bioeconomy.

14European commission (2019), The European Green Deal.

Solutions to today’s plastics problem

Boosting demand for sustainable plastics

In the end, policy intervention in the plastics market boils down to one thing: price. Policy makers can incentivise a switch to sustainable plastics by placing levies and/or taxes on virgin plastics, thus making them more expensive, as well as incentivising the production of sustainable plastics through subsidies. Investment in R&D, for example in chemical recycling or carbon negative plastics produced from atmospheric CO2,15 would help make new sustainable solutions get to the market quicker and push down prices. Subsidies for carbon negative plastics could be particularly interesting to help remove CO2 from the atmosphere and thus combat climate change.

Standards for recycled content in products would likewise boost demand for recycled plastics, thus making collection and recycling more economically viable. Likewise, bans on certain products, such as certain single-use items, would stave off demand for those materials. More extensive Extended Producer Responsibility (EPR) policies would make producers pay for the environmental costs of their products, according to the ‘polluter pays’ principle.

On the business side, industry collaboration and collaboration across the value chain will likewise enable economies of scale and steeper learning curves that will help drive down the costs of sustainable plastics. Several examples of ongoing industry collaboration can be found in the recent PwC report The rise of circularity in energy, utilities and resources. Such initiatives will in turn boost demand for those materials also outside the initial consortium/ collaboration partners. Collaboration between public and private partners is also essential, such as for example through the Circular Plastics Alliance.16

15Opus 12, accessed 02/12/2020: https://www.opus-12.com/case-study/industry

16European Commission, The Circular Plastics Alliance.

A European solution is a first step

The plastics problem is a global problem which will require global solutions. At the same time, given the size of its market and contribution to the plastic problem, Europe has an obligation as well as the means to lead the way. For the EU, the risk of creating free rider problems is much smaller than for a market of a smaller size. The EU is both the world’s third biggest plastics producer and the largest trade block globally. Inside the union the EU already has the power to enforce certain legislation on its Member States, and because of its size it could influence markets globally if it, for example, would also start taxing conventional plastics produced outside of the EU.

In fact there may be comparative advantages for the EU taking a lead. EU companies should in fact benefit from a robust and integrated approach to plastics, including a single market for secondary raw materials and by-products. And while pioneering the plastics transformation comes with research and development costs, Europe could consequently benefit from these investments by exporting its clean-tech solutions.

With its current initiatives, the EU is taking steps to become a front-runner in this area. By increasing re-use, recycling and recycled content in plastics, as well as banning certain single-use plastics, the EU is leading the way in the switch to more sustainable plastics. The newly proposed ‘plastic tax’ is also a welcome step in the right direction.

All in all, the measures the EU is currently taking will push the markets in the right direction, but there are more tools available in the policy toolbox (see Figure 2). Eventually, a combination of several, or all of them, will likely be needed to solve the plastic waste problem both globally and in the EU.17

17In July 2020 the EU announced a new plastic packaging levy to be introduced with effect from 1 January 2021 as part of the coronavirus pandemic recovery package and in line with the EU Green Deal published in December 2020.

What does the Green Deal say about plastics?

The European Green Deal follows up on the EU’s 2018 Plastics Strategy18 and proposes measures to encourage Europe to adopt a sustainable approach to plastics. The European Commission’s ambition is to increase the circularity of plastics in Europe. In the Green Deal some planned areas for intervention are:

- Tackle micro plastics and unintentional releases of plastics, such as for example from textiles and tyre abrasion.

- Ensure that all packaging in the EU market is reusable or recyclable by 2030.

- A regulatory framework for biodegradable and bio-based plastics.

- Measures to regulate single-use plastics.

- Boost the market of secondary raw materials, for example through a requirement for recycled content in products (in packaging, vehicles and construction materials, for example).

- An EU model for separate waste collection aimed to simplify waste management and ensure cleaner secondary materials.

- Rules on waste shipments and illegal exports of plastic waste.

- A new revenue stream (“Own Resources”) based on the non-recycled plastic packaging waste, the so called ‘plastic tax’.

18European Commission (2018), A European Strategy for Plastics in a Circular Economy.

Key take-aways

- There are several policy measures that the EU can use to enable a switch to more sustainable (use of) plastics. Current EU legislation is considering several of them but there are more tools in the policy toolbox which the EU could use.

- Plastic waste is the hidden cost of plastics and it affects companies and consumers alike. The price of pollution needs to be priced in order to create a fully functioning market where sustainable plastics can compete with the conventional ones.

- Industry players need to cooperate more closely across value chains in order to overcome the high transaction costs on the market for sustainable plastics.

- Private actors would also need to cooperate with public institutions and government/ the EU. An example is the Circular Plastics Alliance.

- A robust and integrated single market for secondary raw materials, including plastics, will benefit EU companies in the future. The EU has a chance to become a front-runner in the transition to sustainable plastics.

Follow us