Electrification is not the solution for all sectors

Energy systems integration is the process of coordinating the operation and planning of energy systems across multiple pathways and/or geographical scales to deliver reliable, cost effective energy services with minimal impact on the environment.1 Systems integration focuses on issues such as coupling and optimising the infrastructures for production, transport and storage of energy, finding the optimal transition paths for each.2 It means linking the various energy carriers - electricity, heat, cold, gas, solid and liquid fuels - with each other and with the end-use sectors.

Climate change is in large part a consequence of energy use. Mitigating climate change depends on whether energy use can be reduced, energy can be decarbonised or both. Systems integration will allow optimisation of the energy system as a whole, rather than decarbonising and making separate efficiency gains in each sector independently.3 The system as a whole is central, not the specific parts.

Renewable electricity is expected to decarbonise a large share of the EU’s energy consumption by 2050, but not all of it. Electrification and the use of renewable electricity will play a vital role in decarbonising electricity use in the built environment, (some) road transport and industry, but for many other sectors, a similar decarbonisation will be much harder to achieve. For example, the maritime and aviation transport sectors require high-density energy carriers and certain industrial processes, such as steel making, require high-grade heat. Those are processes that cannot be electrified. In those sectors renewable and low carbon fuels will more likely become the solution in order to decarbonise those processes.

This is where systems integration comes into play: integrating the different energy systems can enable the reduction of greenhouse gas emissions in hard to abate sectors. Here the solution will be to close circles and avoid waste heat, and to use cleaner fuels where electrification is not the solution.

Systems integration is not a solution in itself but an effective means to reach climate and energy targets in a cost-efficient way by using existing infrastructure and cross-cutting solutions.

1International Institute for Energy Integration, Energy Systems Integration: Defining and describing the value proposition, 2016.

2The Dutch research Council (NWO), Energy System Integration

3European Commission, EU strategy on energy system integration

Breaking down silos

For years our energy system was built on several parallel, vertical energy value chains, which rigidly link specific energy resources with specific end-use sectors. To some extent this rigidity is still there. For instance, petroleum products are predominant in the transport sector and as feedstock for industry. Electricity and gas networks are planned and managed independently from each other. Market rules are also largely specific to different sectors.4

Historically this siloed approach made sense since energy production, like much else, was local. Coal, and later oil, was explored and processed locally, and end-use was also local. As shipping costs went down over the decades, infrastructure was gradually built up to ship resources over longer distances. This meant scaling up the same vertical value chains to allow for economies of scale. Power was produced from coal, or from gas, but not from both, because generators could only handle one type of resource.

In the past, prices did not reflect scarcity and prices were set locally by national governments. The gas price was artificially linked to the oil price and there was no price for CO2. In this environment there was no incentive to mix or integrate various resources into one system. Energy provision was very much a political question.

The last decades have seen changes to this. Today, at least for industrial purposes and power production, switching between resources is possible at scale. Electricity can come from a number of different energy sources. Oil can be explored onshore, offshore or from shale, just to name some examples. Globalisation and technological advances have led to market integration, and there are now incentives for companies to look for business cases that integrate various energy sources and systems.

4COM (2020), Powering a climate-neutral economy: An EU Strategy for Energy System Integration.

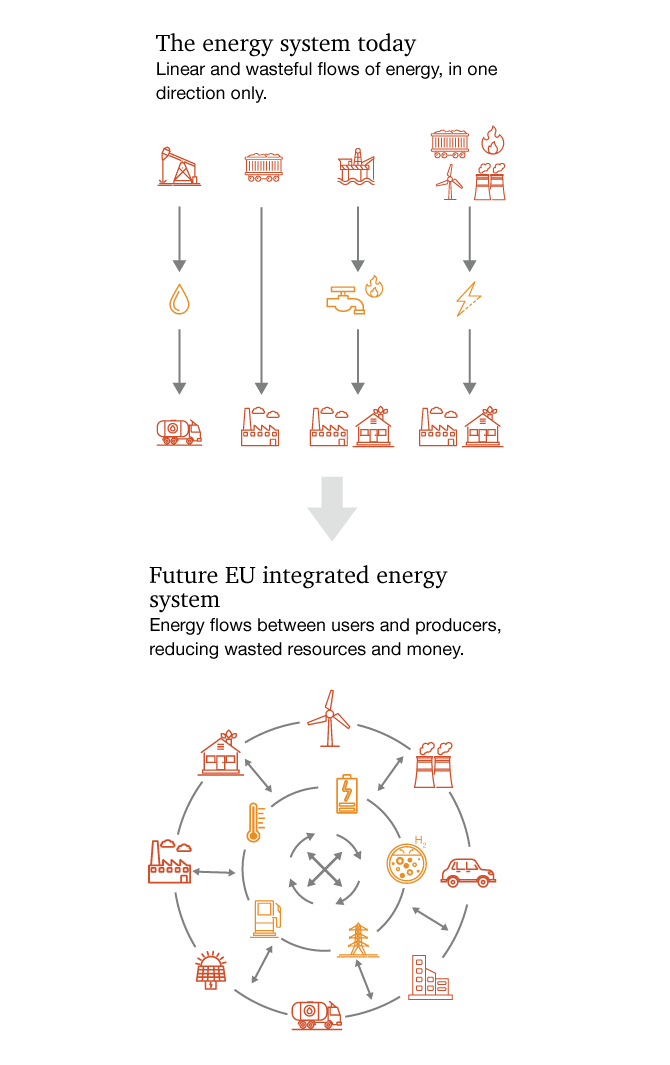

Figure 1: From a linear siloed energy system to a circular integrated one

Source: European Commission

A new energy system

- Sector coupling

- Energy circularity

- Cross-border and cluster collaboration

- The role of hydrogen

Sector coupling

Sector coupling is one key element of energy systems integration. Originally, sector coupling referred primarily to the coupling of energy demand (e.g. transport, domestic heating, and industrial heat and steam) with renewable electricity supply. However, as it is unlikely that all demand can be fully electrified, sector coupling has come to refer to the integrated management of the power and gas sectors, including its infrastructure. This would require cooperation between the transmission system operators (TSOs) of gas and electricity networks. The aim of sector coupling is to optimise the balance between electrification and low-carbon fuels in order to meet energy demand at the lowest societal cost. This means that electrification becomes the solution where this is the most efficient, but low carbon fuels are used where this is the most efficient. Electricity and gas networks would then need to interact with all end uses, i.e. heating, transport, power consumption, feedstock for industry etc.

Sector coupling would result in a more decarbonised environment, by optimising supply according to demand. This would benefit the whole energy system in terms of efficiency. Sector coupling would also reduce the need for infrastructure expansion by introducing conversion technologies, such as power-to-gas installations, at the right locations.5 Existing gas infrastructure could then be used rather than expanding the power infrastructure with high voltage cables.

In order to be successful, sector coupling would need to happen at the local, national and international levels.

5Infrastructure Outlook 2050, TenneT & Gasunie, 2019

Energy circularity

Energy circularity refers to the concept of reusing waste heat and waste streams for energy purposes. This cannot be done without energy systems integration that link energy carriers - electricity, heat, cold, gas, solid and liquid fuels - with each other and with various end-users. This is happening already in combined heat and power plants (CHP), which captures and uses the heat that is a by-product of electricity production (from fossil or biofuels). But it is also happening through the use of waste streams to produce energy, such as biogas produced from organic waste.

A large, yet often unexploited potential is the reuse of waste heat from industrial sites, data centres or other sources. Energy reuse can take place on-site, for example through the re-integration of process heat within a manufacturing plant, or via a district heating and cooling network. To date, 29% of industrial energy demand is wasted, as waste heat is often present at locations where there is no demand for it, or with only expensive and inefficient transport options. Additionally, waste heat temperature is often too low for usage in industrial processes.

However, one example where these challenges have been overcome is in the Swedish city of Luleå which takes advantage of the gases produced in the local steel plant and which is connected to the city’s district heating network. The heat produced can supply the heat demand when temperatures are above -10 degrees Celsius and means that Luleå has the cheapest district heating in Sweden.6

There is however further potential, for example, in energy produced from bio-waste from the agriculture, food and forestry sectors, or from residues from wastewater treatment plants.

6Luleå kommun, 2014.

Cross-border and cluster collaboration

Power systems have increasingly started to operate across borders, mainly for economic reasons. Cross-border and cluster cooperation is important for the whole energy system as no one actor or country will be able to solve the energy transition challenge on their own. As the whole EU needs to become carbon neutral, countries will need to collaborate to reach this goal.

Recently, a new driver for cross-border systems integration has become more relevant: the integration of increasing share of intermittent renewable energy sources. However, this is still happening mostly at a small scale and mainly in the power sector. In order to really achieve a fully integrated European energy system, cross-border integration would need to include the whole energy system, i.e. gas networks, smart grid infrastructure, better supply chains and fuel and electrical charging networks for transport. And it would need a regulatory framework that removes administrative barriers and ensures a level playing field across Europe.

Benefits arise from cross-border collaboration through the more optimal use of existing assets (static efficiency), but also through more optimal investment in production capacities and transmission networks (dynamic efficiency), allowing investment flows to find their welfare maximising routes. Direct benefits will include lower operational costs, decreased fuel costs and decreased balancing costs, and lower costs because of decreased needs for additional investments in transmission and production.

Likewise, collaboration is also about optimising resources. Industrial clusters are groups of often specialised companies and other public or private related supporting actors in a location that cooperate closely. Together, those companies can be more innovative as energy projects will benefit from the different competencies and expertise that each party brings. This works to the benefit of all companies working in the cluster.

The role of hydrogen

Hydrogen, and especially green hydrogen produced from renewable energy,7 is one of the fuels that have one of the highest decarbonisation potentials for hard to abate sectors, but will require systems integration in order to become a viable alternative low-carbon energy source. Hydrogen offers solutions for the hard to abate parts of the transport system, such as the maritime and aviation sectors. Hydrogen can also replace fossil fuels in some carbon intensive industrial processes, such as the steel and chemical sectors.

Additionally, hydrogen has a strong potential to solve the storage issue created by intermittent renewable energy sources (mainly solar and wind) and become a vector for renewable energy storage, alongside batteries. Hydrogen storage would ensure back-up for seasonal variations (that batteries cannot provide) and connecting production locations to more distant demand centres.

Unlike the greening of power – which seems broadly on track – the introduction of more low-carbon fuels such as (blue and green) hydrogen is lagging behind. Fuels are the backbone of the European energy system today and will likely remain so as we move towards 2050. Achieving the EU’s 2050 target will therefore require switching to lower-carbon fuels as a prime policy priority in the current decade. We will explore this topic further in a subsequent issue of our Green Deal Monitor.

7The best known process is electrolysis, in which water (H2O) is split into hydrogen (H2) and oxygen (O2) using green electricity.

The way forward

Creating an integrated European energy system is not going to happen overnight. There are good historical reasons why the energy sector was organised in silos, but it is also clear that this historical heritage has created barriers that prevent energy systems integration from happening at full scale. While energy systems are now more intertwined than before, there is still some way to go.

For instance the divided ownership and opposite interests within the energy sector presents a barrier. The electricity sector, for example, has long been in public hands, while the oil and gas sector has been dominated by privately owned large multinationals. The alignment of interests within the electricity sector has further decreased in the past decades, as Europe (and much of the world) has pursued a strategy of privatisation in order to foster competition. Regulation about the separation of production and trading activities has further increased the complexity.

So, what needs to be done?

To overcome these barriers, companies and governments need to work together. The role of governments and the EU is to create a playing field where interests are aligned and externalities are priced-in, while competition is stimulated. Companies on their hand must dare to look beyond their own short term P&Ls, and instead get creative in order to find common ground to get projects going. Only by widening the perspective, can the socially optimal solutions be realised.

The type of infrastructural challenges we are facing are not new. Europe has been very successful in realising large private initiatives before, and these brought large wealth for companies and society. The railways, gas- and electricity grids are all examples of initially private infrastructure developments, which only later became regulated and government owned.

In the capital intensive and sometimes highly competitive energy sector, European companies can only become successful players in newly emerging areas with some bravery. Going after new chances with only a limited view on the future, but driven by the desire to realise great things. Remember that guy from the US who fully went for electric cars against all odds, also in a highly competitive and capital intensive industry? Nowadays Tesla is one of the most valuable car companies in the world. This puts pressure on all other car manufacturers to accelerate their timelines for electric cars and the company is widely recognised as the great driver of innovation in electric vehicles. Sometimes bold moves pay-off big time.

Two prerequisites to accelerate the energy systems integration

Financing the innovation:

- Companies need to be courageous enough to think outside the box to come up with new business ideas and be determined enough to bridge the ‘valley of death’ when embarking on a new business venture. Companies need to have a well thought through strategy to cover the initial lack of cash-flow before a new product or service can bring in revenue. They also need to widen their perspective and find common ground to team up with other companies or organisations to form partnerships that can better solve challenges at hand and are better positioned to attract funding. In this sense, financing is always the main problem.

- So, companies, governments and the financial sector need to be creative in ensuring financing for the large investments required for the energy transition. For projects which require high investments that cannot be recovered by increased revenues in the short term, setting up an equity fund that has some seed financing from the EU could be an alternative. This could fulfil part of the high demand for low-risk securities with stable cash flows, and create opportunities for institutional investors to participate in sustainable projects that have a high societal value.

Regulating to facilitate the transition:

- Governments and the EU should ensure the adequate pricing of externalities, such as pricing CO2, and solve coordination problems between private actors. Tenders could be organised to offer subsidies and funding to consortia that provide solutions to existing bottlenecks. Like the successful tenders for the offshore wind, these could lead to strong innovation, cost benefits and profitable new industries.

- The currently siloed network operators (TSOs) in Europe need to be driven by similar business incentives. Regulators should encourage closer cooperation between gas and electricity network providers, with a view to create an infrastructure which is as efficient as possible. For example, a similar ownership structure for those entities would better ensure coordinated long-term planning.

Follow us

Contact us

Energy - Utilities - Resources Industry Leader, PwC Netherlands

Tel: +31 (0)61 003 87 14