{{item.videoDuration}}

{{item.title}}

{{item.text}}

{{item.videoDuration}}

{{item.text}}

DSTs are not a corporate income tax, sales tax or a VAT. They are generally a tax on gross revenues that multinationals generate from in scope digital services. The in scope digital services can generally be divided into the following categories:

As DSTs are implemented unilaterally, the details of the rules - such as scope, tax rate, and reporting deadlines - may differ in each country. Most of the countries have included a 3% DST rate on the revenue generated with respect to the in-scope activities.

We are happy to assist you with identifying the consequences of DSTs to your business. Feel free to contact us!

In most countries, DSTs only apply if certain global and local thresholds are met. These thresholds differ per country. Generally, DSTs apply for multinational companies with a global revenue of at least EUR 750 million. The local thresholds differ from approximately EUR 0 to EUR 25 million.

Unlike most other taxes, the country where a company is resident is in principle not relevant when determining whether a company is subject to a DST. In general, the location of the users is decisive when determining which country has the right to levy a DST. How users’ location is determined may differ in each country and for each in scope digital service. Generally, users’ location is determined by way of the IP address or geolocation from a device, the location where the account used on the platform has been logged in etc.

Most countries have taken the position that DSTs are not covered by double tax treaties as they are of the view that it qualifies as an indirect tax. Therefore, countries are not limited in their right to effectuate the DST claim under a double tax treaty. However, most countries allow DST as a deductible expense for corporate income tax purposes.

The levy of a DST in addition to a corporate income tax could lead to double taxation. For example, a company is a tax resident in Country A for corporate income tax purposes and collects and transmits users’ data of users in Country B (without having physical presence in Country B). In this example, the profits on the sale of users’ data is subject to corporate income tax in Country A. In addition, provided that the group where this company is part of meets the DST thresholds, Country B may levy DST on the revenue as well. As a result, double taxation may occur if the DST of Country B will not be considered a deductible expense for corporate income tax purposes in Country A.

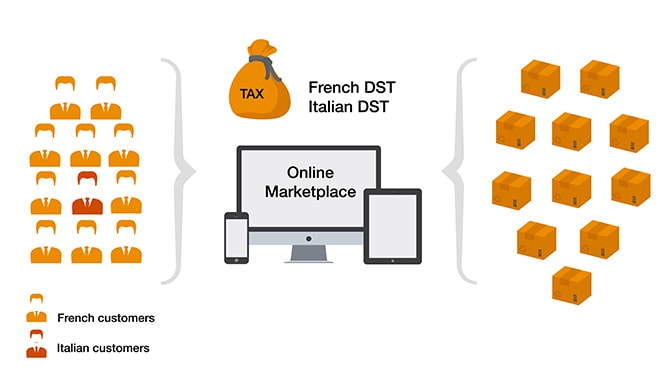

Double taxation could also occur when two countries levy a DST on the same digital service provided by one company as both countries are of the view that the digital service is provided to a user in their country. For example, if a company has an online marketplace which is used by a seller, resident in France, which sells a good to a buyer, resident in Italy. In France, revenues of an online marketplace are in scope of French DST if either the seller or buyer is located in France. In Italy, this transaction would also be in scope of DST because the buyer qualifies as an Italian user of the online marketplace. As a consequence, there is the risk that DST will be levied twice over the revenue generated from the Italian.

In recent years, the taxation of the digital economy has been an important discussion topic. Businesses now regularly perform activities in jurisdictions without maintaining a physical presence (i.e. by not having a legal entity or branch). This may result in misalignment between where value is created for certain (digital) activities and where the current international tax regime allocates the taxing rights. Therefore, the fundamental concepts of tax residence and source on which the current international tax system is based is viewed to be outdated.

The Organisation for Economic Cooperation and Development (“OECD”) is working on proposals to adapt international rules for the taxation of the digital economy on a cooperative basis. In this respect, reference is made “Pillar One and TP”. In addition, the European Commission published two proposals in 2018 as part of the ‘EU Digital Tax Package’ and announced a new proposal regarding a Digital Levy in July 2021. However, the introduction of a separate digital levy in the European Union (“EU”) has been criticized as conflicting with the work by the OECD. The EU therefore decided to hold off on further work on the Digital Levy proposal for now.

Despite the attempts to reach a consensus at a global and/or EU level, international initiatives have not yet led to adjustments of the international rules of taxation of certain digital activities. Therefore, more than twenty countries worldwide (including the UK, France, Italy, Spain, India and Canada) have implemented or proposed to implement a so-called Digital Services Tax (“DST”). These unilateral DSTs are generally meant as an interim solution until there is an agreement at international level for the taxation of income generated by multinational companies with digital services. It is intended to have a coordinated repeal of unilateral measures, such as DSTs, when agreement is reached on OECD/G20’s Pillar One (Pillar One and Transfer Pricing).

{{item.text}}

{{item.text}}

Deputy Global Tax Policy Leader, EMEA Tax Policy Leader, PwC Netherlands

Tel: +31 (0)62 294 38 76