This is according to PwC's Global CSRD Survey 2024. In it, a large majority of Dutch respondents (79 per cent) indicate that they expect to be ready in time to report on their sustainability performance in accordance with the new European directive. The Netherlands scores significantly higher than the average of 63 percent in the survey of more than five hundred companies in more than thirty countries. CSRD stands for Corporate Sustainability Reporting Directive and requires companies to report on non-financial information.

‘Indeed, we see that most companies that start working with the CSRD come to appreciate the rationale behind it more,’ says Alexander Spek, responsible for the Sustainability practice at PwC Netherlands. 'They find it quite a reporting challenge, but they also appreciate the new insights and focus on sustainability topics that may have been underexposed before.'

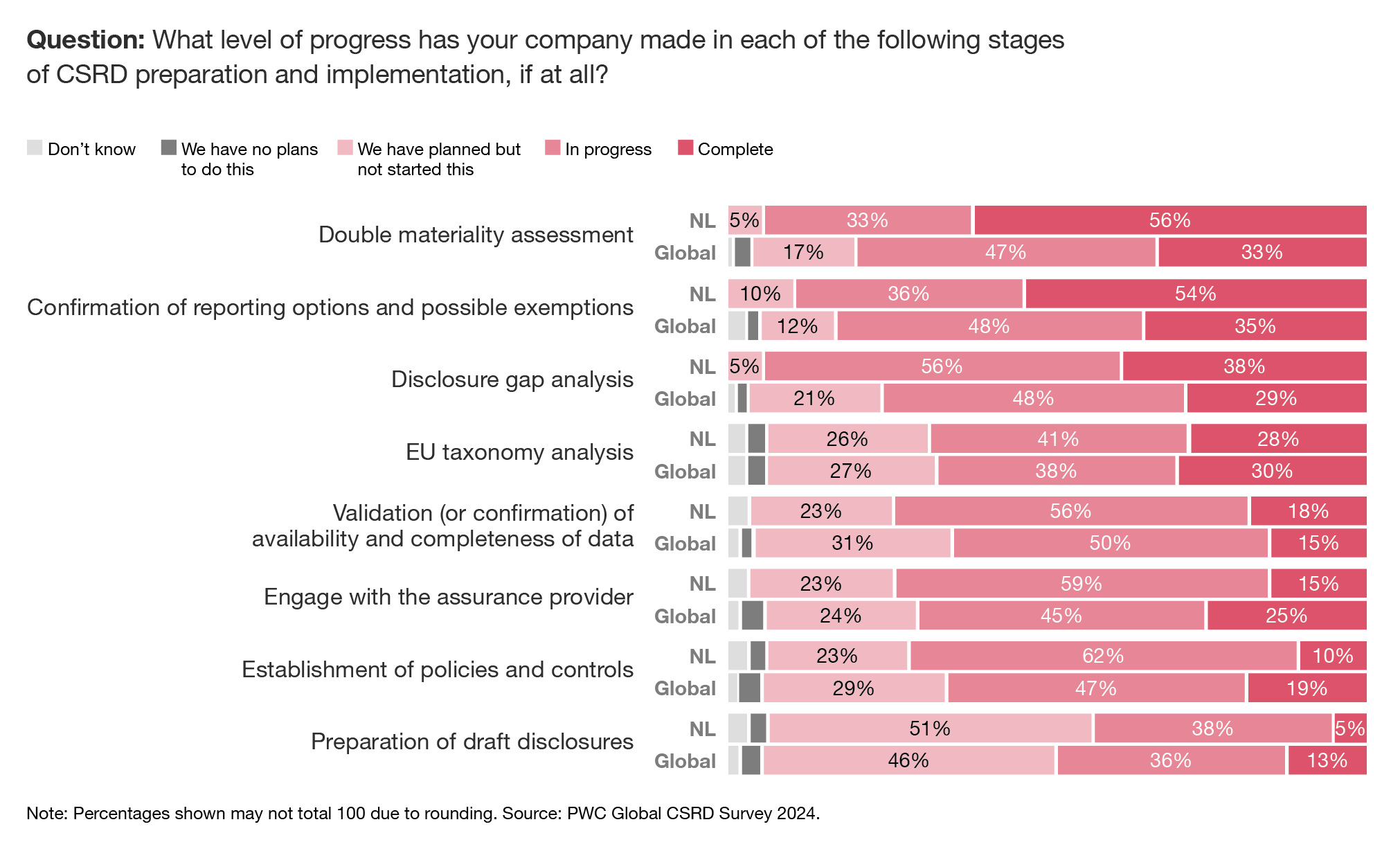

Progress in CSRD implementation leads to optimism

The relatively high level of optimism among Dutch companies about their CSRD implementation is partly based on the progress they have already made. More than half have now completed key preparatory steps: 54 per cent have completed the confirmation of reporting options and exceptions, and another third are in the process of doing so. The mandatory double materiality analysis has already been completed by 64 per cent of the companies surveyed, with another third still working on it.

These results compare favourably with the average scores in the survey: globally, a third of companies have completed these steps and half are still working on them. Dutch companies lag slightly behind in implementing policies and control rules and in writing disclosures for the sustainability report.

Getting a grip on CSRD implementation

The survey results suggest that companies are gradually becoming more confident that they will complete their CSRD implementation correctly and on time. Companies reporting for the first time in 2025 - and therefore presumably further along - are more optimistic than those that do not have to report until 2026. PwC experts also see that companies find the CSRD less daunting once they understand in detail how the reporting standards are structured and what they require.

‘It is good to see that the majority of Dutch companies are really taking up the CSRD challenge,' says Karin Meijer, sustainability reporting specialist at PwC. 'To keep this challenge manageable and to understand exactly what is expected, it is important to start as early as possible with the right team.'

These insights often follow from the preparatory steps mentioned earlier. If a company has determined that it will be reporting at the consolidated group level or at the level of individual entities, it will also be clearer what data is needed, on what topics, from what sources, and within what timeframe. On this basis, teams can draw up concrete work plans and get a grip on further implementation.

More recent sustainability themes remain underexposed

Confidence in being able to meet the CSRD requirements is highest among Dutch companies for several of the more common sustainability themes. When it comes to their own employees, climate change and business behaviour (topics on which many companies already report), more than ninety per cent say they have at least 'some confidence'.

Strikingly, Dutch companies are much more likely to say that a number of sustainability themes on which they report less or are not used to reporting on are 'not applicable' or 'not in scope' for them. Topics such as customers and 'end users', 'pollution', 'impact on communities' and 'biodiversity and ecosystems' are not included in their CSRD reporting, according to between a third and a half of respondents. One explanation may be that Dutch companies set clearer priorities in the double materiality analysis. PwC's experts expect these differences to disappear over time as more consistency emerges across sustainability themes. Dutch companies may then add additional topics to their reports.

Obstacles to CSRD implementation

The fact that companies are generally very confident about the 'successful outcome' of their CSRD implementation and are making progress with it does not mean that they do not have obstacles and challenges to overcome in the process. The availability and quality of data, the complexity of the value chain and the availability of sufficient human resources are mentioned by Dutch companies as the main challenges. For fifty to sixty per cent of respondents, these factors are an obstacle to a great or very great extent.

This is not surprising. The CSRD is so comprehensive that companies need to collect, verify and consolidate many new types of data. Much of this information is often not yet available in existing ERP and other central source systems. These findings are also in line with the average survey results. Only the interaction with other laws and regulations and the involvement of management are perceived as less of a problem by companies in the Netherlands.

CSRD leads to a greater role for sustainability in decision making

PwC's first Global CSRD Survey, not only provides insights into the progress and challenges of implementation, but also gives cause for optimism. At least for the directive's proponents, who hope that transparency in corporate sustainability will lead to more sustainable business operations. Two-thirds of Dutch respondents say that the CSRD makes them take sustainability more into account when making decisions (in addition to the 21 per cent who say they already do so).

This is also reflected in the results on the involvement of different business functions in the CSRD. In addition to the traditional 'sustainability departments', almost all Dutch companies also involve the finance department and members of the board and supervisory board, significantly more than internationally. In almost half of Dutch companies, the finance department is responsible for implementing CSRD, while in others it is mainly the sustainability department.

'In our view, this responsibility should also lie with finance, given its role in external reporting,’ argues PwC expert Willem Jan Dubois. 'However, it is crucial that there is good interaction with those responsible for strategy, sustainability, compliance and the business itself. Only then will you get an accurate and relevant report that the entire organisation can agree on.'

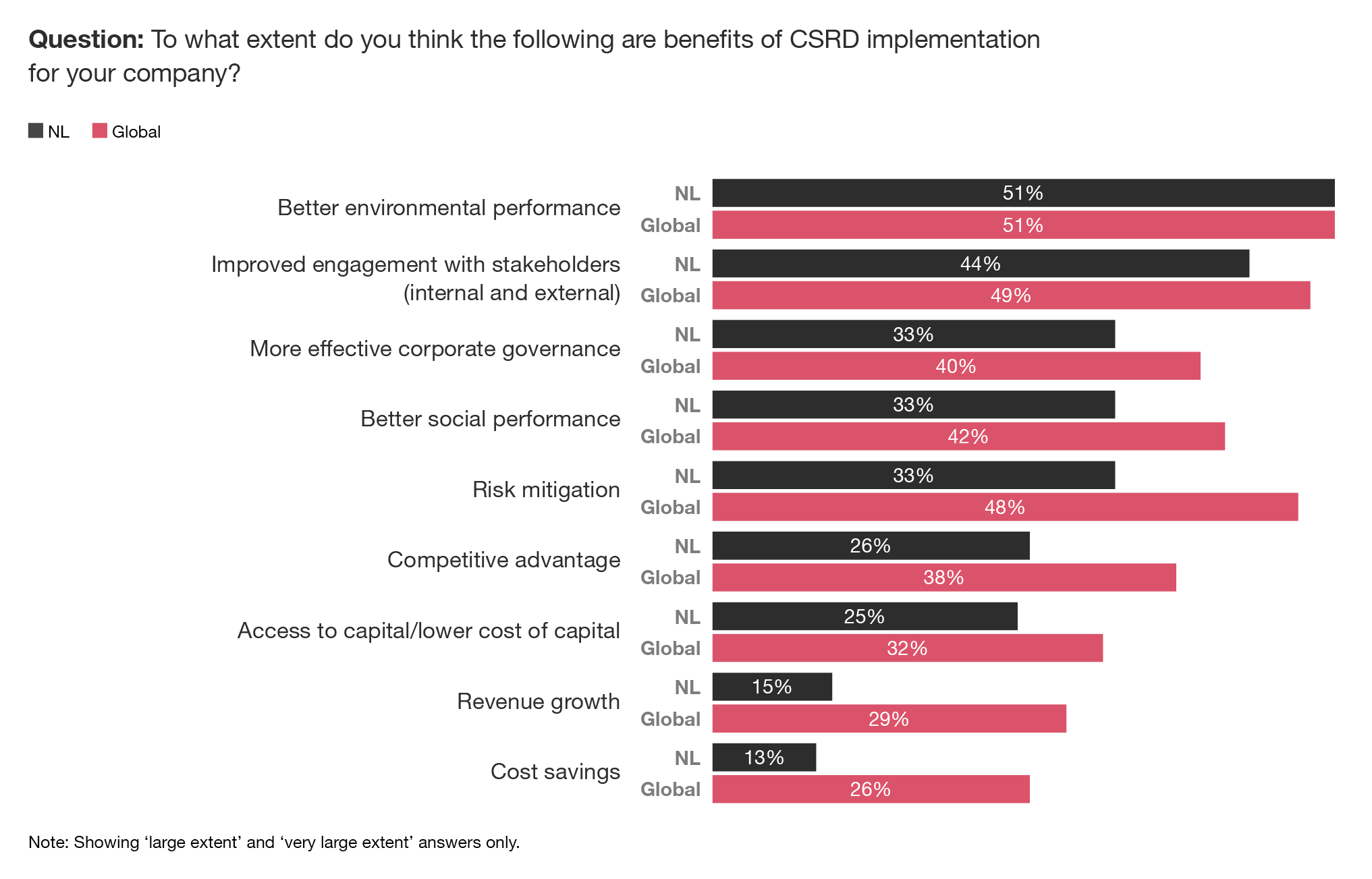

Expected benefits of the CSRD

As with confidence, optimism about the benefits increases as companies progress further in implementing the CSRD. Companies that have to report in 2025 are generally more positive about the benefits of the CSRD than those that do not have to report until 2026. Dutch companies stand out somewhat in this respect: on average, they are less positive about the positive effects of the CSRD than the other respondents. In particular, the majority see benefits in areas clearly related to sustainability: better environmental and social responsibility results, stronger stakeholder involvement, more effective corporate governance and a reduction in sustainability risks. Dutch companies are less convinced than the other companies in the survey that the CSRD will also bring economic benefits: a minority expect their competitiveness, capital costs, turnover and costs will improve.

How to make CSRD implementation a success?

To ensure the success of their CSRD implementation, organisations need to consider a number of points:

- Mobilise a multidisciplinary team representing departments responsible for finance, sustainability, compliance and the business itself.

- Make sure it is clear what is expected of the organisation, including timelines. An essential step in this is the double materiality analysis.

- Define the ambition - and therefore the critical path - for both compliance and strategy: What is the bigger story for our organisation that we want to tell the world about sustainability?

- Pay sufficient attention to one of the main bottlenecks in many CSRD implementations: collecting, verifying and consolidating all the, often new, data required for CSRD reporting.

- Explore the different systems that can help make this reporting process as efficient and effective as possible (and don't forget to look at the financial reporting process).

Read all the Dutch results of PwC's Global CSRD Survey 2024